More of a test post, but this is a climate data marketplace for all the things, (‘green’ tokens, supply chain risk management, impact verifications, parametric/disaster insurance) built on the polygon blockchain, chainlink, advanced satellite monitoring.

Partnership with the country Namibia to monetize their ‘green’ hydrogen energy

A clear example how parametric insurance is a part of the financial apparatuses supporting dataization of everything life ect ect.

Thier lead investor coinfund, based out of nyc and miami, has former blackrock people, big banks ect

So this “green hydrogen” uses electrolysis - that’s where graphene comes in, evidently.

Also what do you make of dClimate? Is this a competitor to the Ocean Protocols out there? I guess we are likely to see many different platforms looking to aggregate and leverage impact data.

I don’t know if Lynn is on here yet, but I see that Mark Cuban is one of dClimate’s advisors. dClimate - Community

Ill need to dig deeper into the specifics about their software and stuff to have an understanding where it stands in relations to ocean protocol, but in general there are definitely more web3 data marketplaces than Ocean, and often those first big efforts end up not being ‘the thing’ and smaller projects make more headway quicker

“Offsets” are just another way of permitting deforestation and pollution. Government permits are about giving permission to environmental harm doers. They sanction the activity with largely fraudulent (because typically unenforceable) regulations on the mere levels are harm “permitted”. Carbon credit markets are also about sanctioning the activity.

Also, so much of this on based on modeling and projections. That’s significant.

I’m not up to speed on parametric insurance though.

Not to volunteer you @leo, but I think a presentation on parametric insurance would be really useful for people.

@Jason_Bosch my sense is that these policies are linked to specifically measurable weather events that will use IoT (satellite, weather measurement tools) to verify things like rainfall and wind speed in a geographic area. If terms of policy are met a payout is made fairly quickly. Blockchain was set up to manage this type of insurance. It’s linked to catastrophe bonds. The One Where Insurance Meets Blockchain and Parametrics | Cassels.com

Looks like the Weather Company has been owned by IBM since 2016.

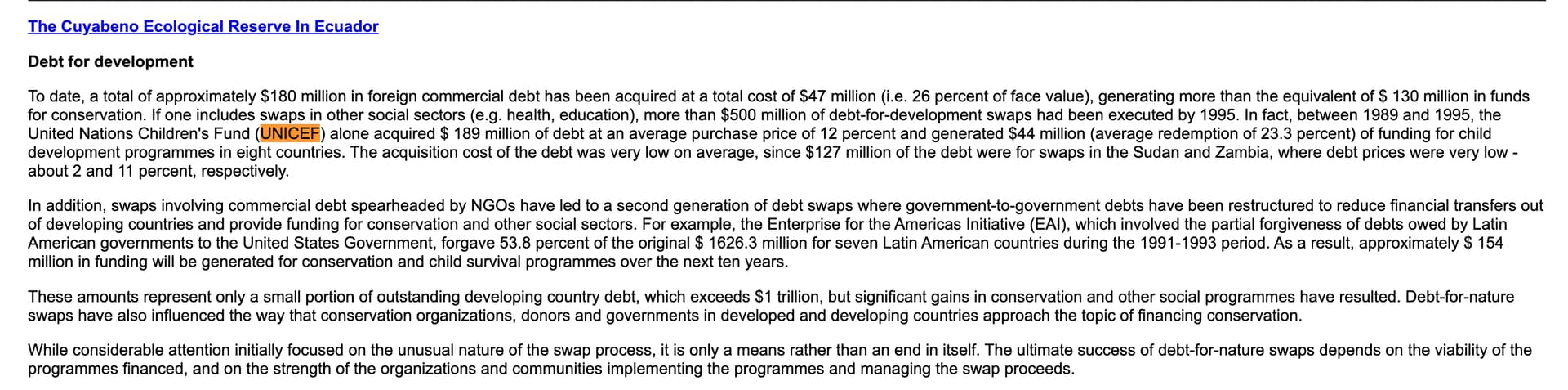

I noticed on the old board as I was moving stuff over that @jenlake mentioned “debt for nature” swaps. I found this old FAO link. I can totally see them engineering / enhancing problematic weather (flooding, hurricanes, wind) patterns to justify the 30x30 reserves for global land / marine management with all the sensors, etc. and states of exception. The bit that stood out for me here was UNICEF’s involvement, too. So use debt / structural adjustment to access not only Global South land but youth, too. Criminal. Unasylva - No. 188 - Funding sustainable forestry - Debt-for-nature swaps: a decade of experience and new directions for the future

I agree and with offsets and tokenized offsets its like making a market for permits, so the conservation, ‘regenerative’ groups can make money ‘earning’ the offsets to sell to deforesting companies.

Alisons comment on parametric insurance sums it up well, but broadly ‘parametric’ insurance just refers to insurance policies that are automatically triggered based on some sort of measurable event. The payout is predefined, based purely on the trigger metric, not on actual damage to property.

I am 90% sure that the first parametric insurance offering were catastrophe bonds in the early 2000s designed through the world bank in Mexico. These were focused on earthquakes, so a certain Richter scale measurement was the trigger for the payout.

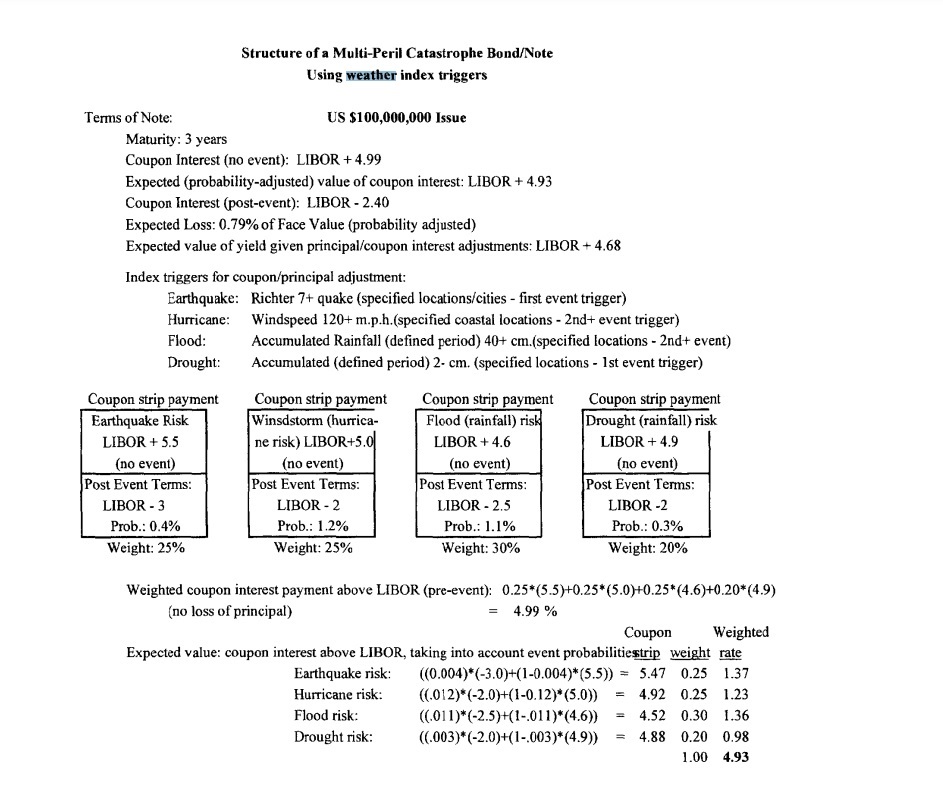

I was looking for the Mexico world bank papers I ahd read before but came across this policy report in 2001. This screen shot shows the structure of the “weather index” product which is a parametric design

Of course the concept seem handmade for the IoT 4IR world of total awareness, sensor networks. There is a growing contingent of smart contract based insurance products which are all parametric.

I do agree, its a more concrete thing that isn’t too difficult to wrap your head around, but when you get it help solidify why there’s so much ‘money’ to be made through sensors everyone on earth.

The news comes as Metabiota commercially launches the industry’s first ever platform for estimating epidemic preparedness and risk, including the frequency, severity, duration and cost of outbreaks. With a powerful combination of epidemic risk analytics, historical data, disease scenarios and insights from public health analysts and global epidemiologists, Metabiota’s platform is enabling the insurance industry to offer new epidemic insurance solutions by delivering capabilities that allow insurers to better understand and underwrite risk.

Described in another article is their parametric insurance product PathogenRX, based on this edpidemic preparedness index

In 2018, Marsh collaborated with Munich Re and epidemic risk modeling firm Metabiota to create PathogenRX, a parametric insurance product designed to protect against the economic impact of infectious disease outbreaks. The product was designed for industries “that depend on people to show up,” like hotels and sporting events, said Christian Ryan, U.S. hospitality, sports and entertainment leader at Marsh. If public anxiety over an outbreak of Zika or Ebola keeps people away, those businesses can fail, and often do so quickly.

The product uses a pathogen sentiment index developed by Metabiota that gauges public fear and behavioral change in the wake of an epidemic outbreak. According to Metabiota CEO Bill Rossi, the index was made possible by advances in disease tracking and reporting, software machine learning and artificial intelligence. https://www.rmmagazine.com/articles/article/2019/04/01/-The-Evolution-of-Parametric-Insurance-

wonder what the pay out like… ill add if I can find info on that

Wow this is really interesting, so the triggers in the case of PathagenRX were:

A public health outbreak can lead to loss of gross profits, loss of revenue, and extra expense. PathogenRX can provide coverage for such losses incurred as a result of an infectious disease event in a designated geographical coverage area. Coverage is typically based on three straightforward triggers:

1. The World Health Organization (WHO) issues a Disease Outbreak Notice (DON) during the policy period. 2. The WHO issues a Public Health Emergency of International Concern for the disease specified in the DON. 3. A civil authority orders restrictions — including sheltering-in-place or partial or full cessation of business — for the area covered by the policy or a respective cluster of the insured’s property.

All three triggers must be satisfied for the policy to respond.

Thanks for checking it out - the linked paper in there, Susan Erikson’s “Faking Global Health” from 2019 is an important read in terms of how they have and will game the “risk” metrics. Full article: Faking global health

Adding more. So dClimate was created by the founders of insura tech/data annalytics company Arbol. “dClimate is the culmination of Arbol’s work in building a decentralized, blockchain based data network over the past two years.” From what I am gathering dClimate is used in all of their weather related products.

Arbol is fairly large, 70 million in ‘gross premiums’ in 2021. Pretty sure that refers to the total amount paid by customers for coverage.

Mubadala UAE sovereign wealth fund type thing, their venture capital arm invested in Arbol. Allison mentioned Mark Cuban, hes an advisor and investor

So in 2020 they ran this piolet with HAnnover RE and Global Parametrics. Im putting this here because Hannover Re is also part of the Lemonade Crypto Climate Coalition, a consortium of fintec/web3/insurance companies building a DAO based parametric insurance offering for small farmers. I have been looking into that group since it was announced.

for tokenized natural credits (right now carbon, sattlities useing a mixture of optical microwave and other wavelengths can mapp much of the forest in detail which they use to calcucate the amount of carbon it pulls in)

risk assesment in commodity production (in the presentation he goes into how its used in coffee). But also things like predicting construction delays and whatnot

And its not something in development or a pitch, its basically the basis for many of Arbols insurance products.

But they showed different non insurance uses in the presentation, and apperently are working with forgien govts

" In Africa, there are far fewer weather monitoring stations on the ground than in Europe or the US, and almost 90% less than the minimum recommended by the World Meteorological Organization. This absence of data means weather forecasts are often inaccurate, and there are barely any early-warning systems for cyclones, droughts, and intense floods."

I can’t help but imagine how all the surveillance infrastructure they have planned for “weather” will play into Hoskinson/Cardano’s vision to overtake Africa.

“You can also directly invest in projects, tokenize that project and then basically earn all the yield that project earns over time right? The same you could buy some land then earn all the yield that the different projects that you may develop over time plus the the appreciation and value of the land and you tokenize that and capture that. With this approach you need to be super super careful about neocolonialism and like a um being sure to involve the local community, right? Um and this needs to be part of the solution anyway uh every time because otherwise it’s not not safe as an as green asset class right?”

This statement is astounding to me in so many ways. He openly acknowledges neocolonialism, which is precisely what this is, but then gives some lip service to “involve the local community” because otherwise it’s “not safe as a green asset class.” Presumably because of how it will be perceived, not what it actually is.

And I’m convinced that most of these pitch men and women for these schemes genuinely see themselves as enterprising do-gooders. We’re not dealing with a problem of knowledge so much as we are dealing with a very harmful market and data theology.

One of the member so of the lemonade coalition is this insuratech company Pula. The founder was the director of the Syngenta foundation Rose Goslinga, where they did some of the first mobile based crop insurance targeting small farmers (with safricom). Acre Africa came out of their program. Syngenta is basically owned by the Chinese government, which provides an interesting interface where USAID and western agricultural forces are working with the Chinese

I need to do more digging into Cardano, but with blockchain based insurance I haven’t seen any projects from Cardano yet tbh.

-- Sid Jha")